Apple Pay in India: Can RBI work around their 2FA policy?

2026-04-15

What is Apple Pay? Is it better than UPI?

Mumbai- Ten years ago when India faced major demonetization, major reforms had to be made. To avoid the flow of black money and to make sure transactions became more transparent, the Indian government developed a UPI concept. UPI stands for United Payments Interface. It is a seamless payment ecosystem. A crisp, structured way of making contactless payments. UPI has amassed widespread national and global success in specific countries.

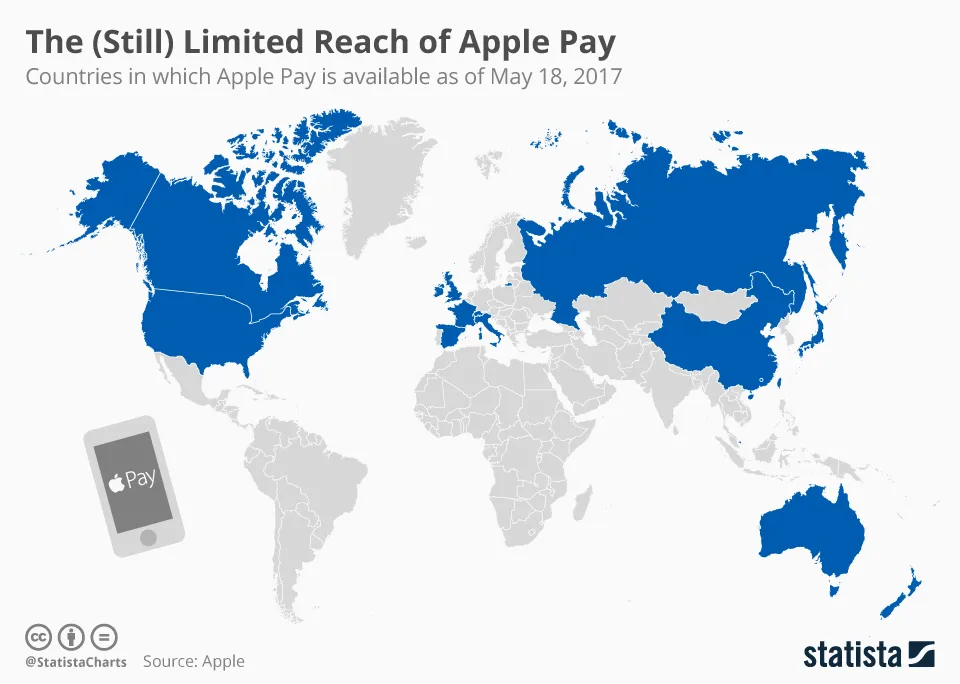

Now let’s take a deep dive into Apple Pay, Apple’s take on seamless, secure payments. It is a mobile payment service by Apple that allows users to make payments in person, in iOS apps, and on the web. Supported on iPhone, Apple Watch, iPad, Mac, and Vision Pro, Apple Pay digitizes and can replace a credit or debit card chip and PIN transaction at a contactless-capable point-of-sale terminal. It was launched on October 20, 2014, alongside iOS 8.1. Announced on September 9, 2014, it was introduced by Apple to enable contactless, NFC-based payments using the iPhone 6 and later models.

UPI is generally better for the Indian market due to its near-universal acceptance, direct bank-to-bank transfers, and zero-fee structure, whereas Apple Pay offers faster, contactless biometric convenience suitable for higher-end merchant environments. UPI dominates the ecosystem, making it more practical for daily use, including micro-transactions.

Despite these differences, there could be a possibility where Apple Pay makes amends as per RBI’s policies, since India’s online payment market, Gen Z being the main driving force, is too good to miss.

Understanding RBI’s 2FA Mandate & Possible Workarounds:

The RBI's 2 Factor Authentication mandate, effective April 1, 2026, requires all domestic digital payments (UPI, cards, wallets) to use two distinct, independent authentication factors. At least one factor must be dynamic (unique to the transaction), aiming to reduce reliance on SMS-OTP and combat fraud by ensuring a single compromised factor cannot bypass security.

In most countries, Apple Pay is designed around seamless, near-instant payments using device-based authentication such as Face ID or Touch ID. While this is technically a form of 2FA (device + biometric), it doesn’t always align with RBI’s interpretation, which often expects an additional, transaction-specific authentication like an OTP.

This mismatch creates a regulatory gap: Apple prioritizes frictionless user experience, while the RBI prioritizes explicit, multi-step verification.

What are some potential workarounds?

There are a few possible paths Apple could explore to comply with RBI norms without completely sacrificing its user experience:

OTP Integration at Checkout

Apple could incorporate an OTP step for Indian transactions. While compliant, this would disrupt the seamless flow that defines Apple Pay globally.UPI Integration

A more localized approach would involve integrating with UPI, allowing Apple to ride on an already RBI-compliant infrastructure. This could mean positioning Apple Pay more as an interface layer rather than a standalone payment system.Tokenization + Additional Verification

Apple already uses tokenization to secure card details. Pairing this with an RBI-approved second factor (like a dynamic PIN or bank-side authentication) could bridge the compliance gap.Bank Partnerships

Collaborating closely with Indian banks to handle the second authentication layer externally could allow Apple to maintain its front-end experience while meeting backend regulatory requirements.

A major challenge: UX vs. compliance:

The Apple Pay Experience: Built on Simplicity

Apple Pay’s global success is rooted in speed and minimal friction. A typical transaction involves a quick double-click, biometric authentication (Face ID or Touch ID), and instant payment. There are no OTPs, no redirects, and no additional steps—just a smooth, almost invisible process. This simplicity is not accidental; it’s central to Apple’s design language.

RBI’s Compliance Requirements: Security First

In contrast, RBI regulations emphasize explicit, multi-step authentication. Transactions often require an additional factor like an OTP or bank PIN, even after device-level authentication. The goal is clear: ensure every transaction is independently verified to reduce fraud risk.

While effective, this introduces friction—something Apple has spent years eliminating.

Where the Conflict Lies

The clash between UX and compliance becomes evident in three key areas:

Extra Steps vs Instant Payments

Adding OTP verification interrupts the seamless flow, making Apple Pay feel no different from traditional payment apps.Consistency vs Localization

Apple typically maintains a uniform experience worldwide. Adapting specifically for India could fragment that consistency.Control vs Collaboration

Apple prefers end-to-end control of its ecosystem, but RBI compliance may require deeper reliance on banks or local systems like Unified Payments Interface.

The Risk of Over-Compromise

If Apple adds too many compliance layers, it risks losing what makes Apple Pay attractive in the first place. A slower, more complex version may struggle to compete with already dominant and highly optimized local solutions.

The Strategic Dilemma

Apple faces a classic trade-off:

Prioritize UX → Maintain global standards but stay locked out of India

Prioritize Compliance → Enter the market but dilute the product experience

Finding a Middle Ground

The most viable path forward may lie in smart integration—leveraging existing compliant systems like UPI while keeping Apple’s interface clean and intuitive. This would allow Apple to meet regulatory expectations without fully sacrificing its UX edge.

In the end, success in India will depend on how well Apple balances these competing priorities, because in this market, compliance isn’t optional, and user expectations are already sky-high.

Global Precedents: How Apple Handles Regulations Elsewhere:

Apple has rarely taken a one-size-fits-all approach when it comes to regulation. While Apple Pay is known for its consistency, Apple has shown a willingness to adapt—quietly but strategically—when entering tightly regulated markets.

Europe: Navigating Strong Data and Payment Laws

In regions governed by frameworks like PSD2 (Revised Payment Services Directive), Apple has aligned with strict authentication rules, including Strong Customer Authentication (SCA). This often mirrors 2FA requirements, where users may need additional verification beyond biometrics for certain transactions.

Rather than resisting, Apple worked within the system—partnering with banks and ensuring compliance while keeping the front-end experience largely intact.

China: Deep Localization Through Partnerships

In China, Apple took a different route. Instead of pushing its own payment rails, it integrated with local networks like UnionPay. This allowed Apple Pay to function within China’s existing financial infrastructure while meeting regulatory expectations.

The key takeaway: Apple compromised on backend control to gain market access.

United States: Operating with Greater Flexibility

In the United States, Apple benefits from a relatively flexible regulatory environment. Here, its native model—biometric authentication combined with tokenization—fits comfortably within industry standards, allowing it to deliver its ideal user experience without major compromises.

What These Markets Reveal

Across these regions, a pattern emerges:

Apple does adapt, but often behind the scenes

It prefers partnerships over structural overhauls

It maintains a consistent front-end UX, even if backend systems differ

Implications for India

India presents a unique challenge. Unlike other markets, the Reserve Bank of India enforces highly explicit authentication requirements that directly impact the user journey—not just backend processes.

If Apple follows its global playbook, it may:

Partner with local banks or fintech systems

Integrate with Unified Payments Interface

Adapt authentication flows specifically for India

The Bottom Line

Apple’s history shows that it is willing to bend—but rarely break—its core philosophy. The company adapts just enough to enter a market, while preserving the experience that defines its ecosystem.

Whether that balance is achievable in India remains the key question.

Future Outlook: Entry, Adaptation, or Exit?

As India continues to dominate global digital payments growth, the absence of Apple Pay raises a critical question: will Apple eventually enter, adapt, or stay out altogether?

Scenario 1: Market Entry Through Adaptation

The most likely path is a localized entry. Apple has historically shown it can adapt when the opportunity is too large to ignore. In India, that would mean aligning with the Reserve Bank of India and potentially integrating with Unified Payments Interface.

This approach would allow Apple to:

Leverage India’s existing payment infrastructure

Stay compliant with 2FA requirements

Enter the market without rebuilding from scratch

However, this would also mean compromising on its tightly controlled ecosystem—something Apple does cautiously.

Scenario 2: A Hybrid Model

Apple could introduce a modified version of Apple Pay tailored specifically for India. This might include:

Additional authentication layers (OTP or bank-side verification)

Deeper partnerships with local banks

A slightly altered UX that balances compliance with simplicity

This “middle ground” strategy aligns with how Apple has handled markets like China and Japan, adapting the backend while keeping the interface familiar.

Scenario 3: Strategic Delay

Another realistic outcome is continued delay. Apple may choose to wait for:

Regulatory evolution or relaxation

Greater alignment between biometric authentication and RBI standards

A clearer pathway that doesn’t significantly dilute its product

Given Apple’s premium positioning, it doesn’t rely on India as heavily as mass-market players, allowing it to be patient.

Scenario 4: Staying Out of the Market

While unlikely long-term, Apple could choose to remain absent if compliance requirements fundamentally clash with its product philosophy. India’s payments space is already dominated by fast, efficient, and widely adopted solutions, leaving little room for a compromised Apple Pay experience.

What Will Likely Happen?

The most probable outcome is adaptation, not avoidance. India represents too large and influential a market to ignore, especially as digital payments continue to expand.

The real shift will come when Apple decides the trade-off is worth it, when entering India, even with compromises, delivers more value than staying out.

Final Thought

For Apple, India isn’t just another market, it’s a test of flexibility. Whether it chooses entry, adaptation, or delay, the decision will signal how far the company is willing to go to balance innovation with regulation in one of the world’s most complex fintech landscapes.

Conclusion: Innovation vs Regulation in India’s Fintech Space

The future of Apple Pay in India reflects a larger balance between innovation and regulation. While Apple prioritizes seamless payments, the Reserve Bank of India focuses on security and trust.

With systems like Unified Payments Interface already thriving, Apple will need to adapt not just launch, to succeed. Ultimately, growth in India depends on blending global innovation with local rules.

-Siddhant Kohli

Stay updated with our latest news and articles. Join our newsletter!

Trending Now

No trending posts found.